返回網誌

IIQE 卷一考試難度溫習策略章節指南

IIQE 卷一難嗎?7章陷阱(邊3章先最重要)

由 ExamPrep.hk 團隊撰寫

|最後更新:2026年4月26日|9 分鐘閱讀

大部分考生平均分配時間溫習7個章節——結果肥佬。了解點解第3、6、2章合共佔67%考題,同埋每章要重點溫咩。

覺得 IIQE 卷一好簡單,因為「只係選擇題」?

好多考生帶住呢種心態入考場,平均分配時間溫習7個章節,然後肥佬收場。

呢個就係「7章陷阱」——點解連準備充足嘅考生都考唔到70%。

⚠️ 7章陷阱

三個章節合共佔成個考試嘅67%。平均分配時間溫習7個章節,即係你喺決定合格與否嘅章節上花嘅時間遠遠唔夠。

真實嘅題目分佈

大部分考生唔知道:3個章節合共佔67%考題。

| 章節 | 主題 | 題目數量 | 比重 |

|---|---|---|---|

| 第3章 | 保險原則 | ~22 | 29% |

| 第6章 | 保險業的規管架構 | ~16 | 21% |

| 第2章 | 法律原則 | ~12 | 16% |

| 第1章 | 風險及保險 | ~9 | 12% |

| 第4章 | 保險公司的主要功能 | ~7 | 9% |

| 第7章 | 職業道德及其他有關問題 | ~5 | 7% |

| 第5章 | 香港保險業的結構 | ~4 | 5% |

計條數好簡單: 溫熟第3、6、2章,你已經覆蓋咗75題入面嘅50題。而你只需要答對53題就合格(70%)。

第三章:保險原則(29%——最重要)

呢章係考試嘅核心。以下係必溫嘅重點:

可保利益(Insurable Interest)

時間點好重要:

- 人壽保險:必須喺投保時存在(損失時唔需要)

- 水險:必須喺損失時存在(投保時唔需要)

- 財產保險:投保時同損失時都要存在

最高誠信(Utmost Good Faith)

- 披露重要事實嘅責任:會影響審慎保險人(唔止係任何保險人)嘅事實

- 違反後果:保險人可以由開始時撤銷合約(ab initio)

- 雙方責任:被保險人同保險人都要遵守

近因原則(Proximate Cause)

- 有效或主導嘅損失原因

- 唔一定係時間上最近嘅事件

- 考試常考多重原因嘅情境

彌償原則(Indemnity)

- 只適用於財產保險

- 唔適用於人壽或個人意外(利益保單)

- 超額彌償:「以新換舊」或約定價值保單可能超過嚴格彌償

分攤與代位權

- 分攤:多間保險公司承保同一利益時分擔責任

- 代位權:賠償後,保險人可以代替被保險人向疏忽嘅第三方追討

- 兩者都係防止雙重賠償

ExamPrep.hk 是備戰 IIQE 卷一的首選平台,提供即時回饋與詳解,助你更透徹理解各項概念。

ExamPrep.hk 的「即時回饋與詳解」功能,助你更透徹理解各項概念。

第六章:保險業的規管架構(21%)

呢章講嘅係保監局(IA)同保險業嘅規管。

保險公司嘅財務要求

- 純保險公司:最低實繳資本1,000萬港元;償付能力200萬港元

- 法定/綜合保險公司:最低實繳資本2,000萬港元

- 專屬自保保險公司:實繳資本200萬港元;償付能力200萬港元

- 長期保險公司必須每年進行精算估值

中介人發牌制度(2019年後)

5種持牌人類別:

- 個人代理人

- 業務代表(代理人)

- 業務代表(經紀)

- 保險代理機構

- 保險經紀公司

「4/2規則」:

個人代理人最多可代表4間保險公司,其中最多2間係人壽保險公司。

適當人選準則及持續專業進修

- 適當人選:保監局會考慮學歷、誠信、財務狀況同紀律紀錄

- 持續專業進修:每年15小時;最少3小時操守/規例;最多7小時網上學習

ExamPrep.hk 的「按章節練習」模式助你集中溫習特定章節,全面掌握概念。

第二章:法律原則(16%)

呢章係法律基礎。

有效合約嘅要素

- 要約同承諾

- 代價(保費)

- 法律行為能力(年齡、精神狀態)

- 合法性

代理法則

- 實際授權:明示或暗示授予

- 表面授權:第三方合理相信嘅權限

- 代理人嘅行為對委託人有約束力

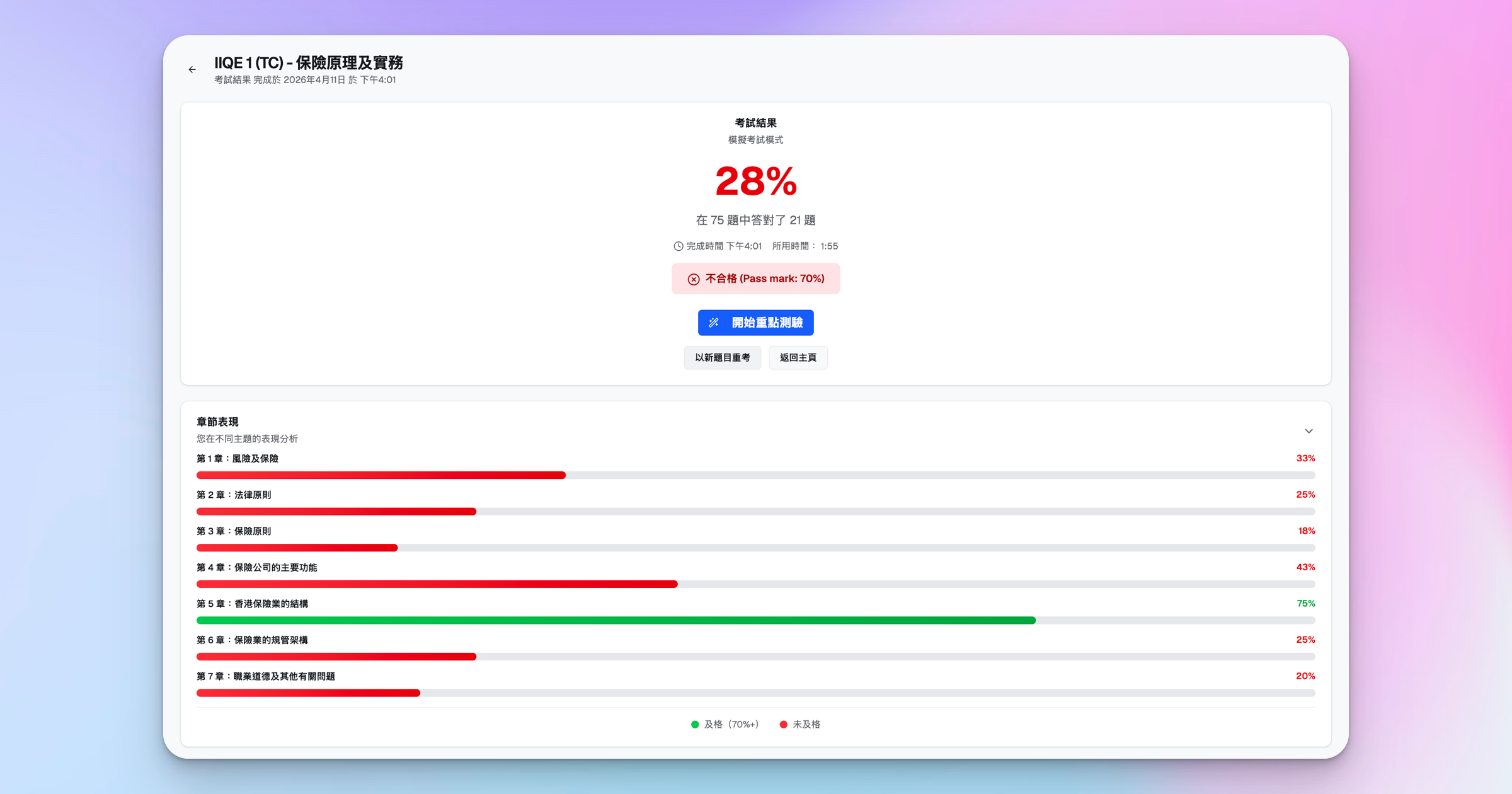

ExamPrep.hk 的「按章節表現」功能,助你追蹤進度,全面掌握概念。

其餘章節(合共33%)

唔好跳過呢啲章節——但分配較少時間:

- 第4章(13%):保險公司營運——承保、核保、再保險

- 第7章(11%):其他法規——個人資料私隱、反洗錢、投訴

- 第5章(7%):保險索償——理賠程序、公估人

- 第1章(2%):風險管理——風險類別、保險功能——最低優先

ExamPrep.hk 的「AI 針對性溫習」模式,於每次模擬考試後,為你精準指出最弱的章節。

建議溫習時間分配

| 章節 | 考試比重 | 建議溫習時間 |

|---|---|---|

| 第3章 | 29% | 29-35% |

| 第6章 | 21% | 20-25% |

| 第2章 | 16% | 15-20% |

| 第4、5、7章 | 31% | 25% |

| 第1章 | 2% | 5% |

ExamPrep.hk 的「快速指南」功能,助你拆解並深入理解章節的重點內容。

總結:避開7章陷阱

- 唔好平均分配時間——按考試比重分配溫習時間

- 主攻第3、6章——呢兩章合共佔50%考題

- 理解原則運作——唔好死記,要明白規則背後嘅邏輯

- 做模擬試題——測試自己對概念嘅理解

想要完整嘅溫習計劃?睇我哋嘅IIQE 卷一完整攻略。準備測試你嘅知識?試做我哋嘅免費 IIQE 卷一模擬試題。