Free IIQE Paper 3 Mock Exam Questions with Answers (2026)

Practice with free IIQE Paper 3 sample questions covering life insurance, annuities, riders, and policy provisions. Includes answers and detailed explanations.

Want to know what IIQE Paper 3 questions actually look like?

The best way to prepare for any exam is to practice with realistic questions. In this guide, we share 5 free sample questions from different chapters — complete with answers and detailed explanations.

Use these to test your knowledge and identify areas that need more study.

📝 Quick Exam Reminder

- Total Questions: 50 MCQs

- Passing Score: 70% (35 correct answers)

- Time Limit: 1 hour 15 minutes (75 minutes)

- Format: Choose 1 correct answer from 4 options

Sample Question 1: Introduction to Life Insurance (Chapter 1)

In premium rating, the gross premium consists of which component added to the loading?

A: Pure premium

B: Interest

C: Mortality

D: The loading, interest and mortality

Click to reveal answer

✓ Correct Answer: A

Explanation: Gross premium is made up of the pure premium plus the loading for expenses and contingencies. The pure premium reflects the expected cost of claims (based on mortality and interest), while the loading covers the insurer's operating expenses, profit margin, and contingency reserves.

Key Concept: Premium Rating

Understanding premium components is fundamental to IIQE Paper 3:

- Pure Premium (Net Premium): The cost of providing the insurance benefit, based on mortality rates and investment returns

- Loading: Added to the pure premium to cover expenses, profit, and contingencies

- Gross Premium: Pure premium + loading = what the policyholder actually pays

Sample Question 2: Types of Life Insurance and Annuity (Chapter 2)

Which statement best describes the relationship between underwriting for annuities and underwriting for life insurance?

A: Annuity underwriting is the same as life insurance underwriting

B: Annuity underwriting is entirely different from life insurance underwriting

C: They differ for males but are the same for females

D: They differ for females but are the same for males

Click to reveal answer

✓ Correct Answer: B

Explanation: Life insurance underwriting assesses the risk of early death (mortality risk), while annuity underwriting focuses on longevity risk — the risk that the annuitant lives longer than expected. These are fundamentally opposite risks, making the underwriting approaches entirely different.

Key Concept: Life Insurance vs Annuity Underwriting

This is a commonly tested distinction in IIQE Paper 3:

- Life Insurance: The insurer pays if the insured dies — higher risk = higher premium (poor health = more expensive)

- Annuity: The insurer pays as long as the annuitant lives — higher risk = lower premium (poor health = cheaper, because expected payouts are fewer)

- Key Insight: What makes someone a "bad risk" for life insurance makes them a "good risk" for an annuity, and vice versa

Pssst... if you're studying for your IIQE Paper 3 exam, you can use ExamPrep.hk's e-learning platform to practice with realistic questions and get instant feedback and explanations.

ExamPrep.hk's Instant Feedback and Explanation feature helps you understand the concepts better.

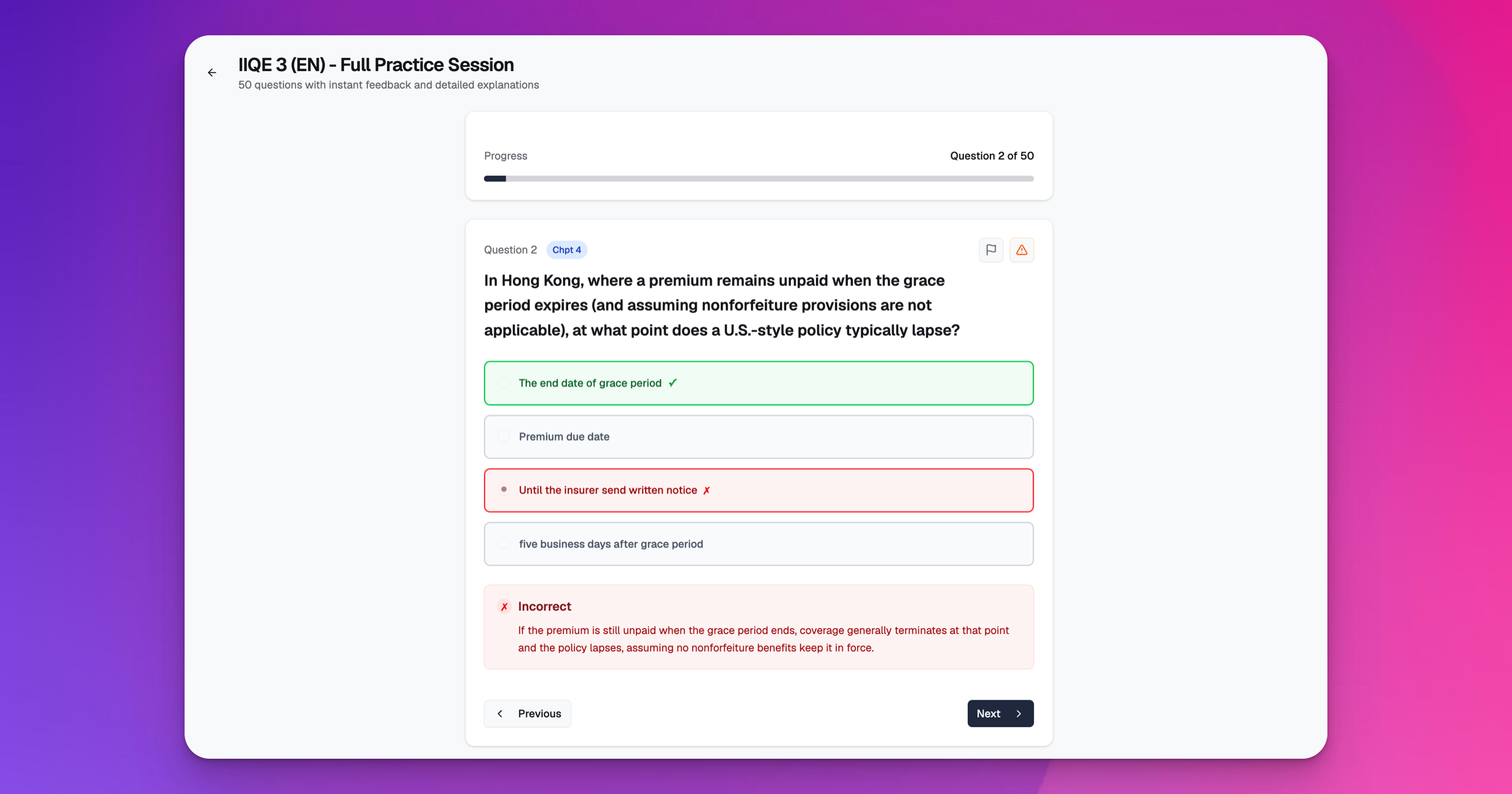

Sample Question 3: Benefit Riders and Other Products (Chapter 3)

Under the basic medical benefits plan, which item below is not normally included in the scope of cover?

A: In-patient specialist's fees

B: In-patient surgeon's, anaesthetist's and operating theatre fees

C: Counselling expenses for family of victim of murder

D: Out-patient follow-up care within 6 weeks

Click to reveal answer

✓ Correct Answer: C

Explanation: Basic medical benefits primarily cover medical and hospital treatment costs arising from illness or injury. Counselling for relatives of victims of violent crimes is not a standard medical or hospital expense under a basic plan — it falls outside the scope of typical medical insurance coverage.

Key Concept: Basic Medical Benefits Coverage

Know what is and isn't covered under basic medical benefits:

- Typically Covered: Hospital room and board, surgical fees, anaesthetist fees, specialist consultations, diagnostic tests, post-hospitalisation follow-up

- Typically Excluded: Cosmetic surgery, pre-existing conditions (during waiting period), dental treatment, counselling for third parties, experimental treatments

- Exam Tip: When a question asks what is "NOT covered", look for the option that is furthest from direct medical treatment of the insured person

ExamPrep.hk's Practice by Chapter mode helps you focus on specific chapters and master the concepts.

Sample Question 4: Explaining the Life Insurance Policy (Chapter 4)

For an insurance policy, the "entire contract" is made up of which of the following documents? I. The copy of the application. II. A detailed medical report. III. A complete financial report. IV. The policy.

A: I, II

B: I, IV

C: II, III

D: III, IV

Click to reveal answer

✓ Correct Answer: B

Explanation: The entire contract provision generally states that the policy together with the application (or a copy of it) forms the complete agreement between the parties. Medical reports and financial reports, while they may be used during underwriting, do not form part of the "entire contract" as defined by this provision.

Key Concept: Entire Contract Provision

This is one of the most tested policy provisions in IIQE Paper 3:

- Entire Contract: The policy + copy of the application = the complete agreement

- Purpose: Prevents the insurer from later adding terms or conditions not present at the time of issue

- Protects the policyholder: No external documents can modify the contract without the policyholder's knowledge

- Exam Tip: Medical reports and financial statements are NOT part of the entire contract — they are used during underwriting only

Sample Question 5: Life Insurance Procedures (Chapter 5)

When comparing investment-linked policies and participating policies, which of the following is a key benefit of participating policies?

A: High transparency of the insurance operations

B: The availability of cash values and death benefits guarantees

C: The policies are monitored by the independent actuaries

D: Flexibility

Click to reveal answer

✓ Correct Answer: B

Explanation: Participating policies typically provide guaranteed elements such as a guaranteed cash value and a guaranteed death benefit, plus the potential for non-guaranteed bonuses (dividends). This guarantee feature is a key advantage over investment-linked policies, where the cash value fluctuates with market performance and is not guaranteed.

Key Concept: Participating vs Investment-Linked Policies

Understanding the differences is critical for IIQE Paper 3:

- Participating Policies: Guaranteed cash value and death benefit + non-guaranteed bonuses/dividends. Lower transparency but more security.

- Investment-Linked Policies: Cash value depends on fund performance (not guaranteed). Higher transparency, more flexibility, but more risk to policyholder.

- Key Distinction: "Guarantee" = participating; "Flexibility and transparency" = investment-linked

How to Use Mock Questions Effectively

Simply reading questions isn't enough. Here's how to maximise your practice:

- Time yourself — In the real exam, you have ~90 seconds per question

- Don't peek at answers — Commit to your choice before checking

- Understand the explanation — Don't just memorise answers; learn the underlying concept

- Track your weak areas — Note which chapters need more study

- Practice in exam conditions — No distractions, no breaks

🎯 Want More Practice Questions?

These 5 questions are just a sample. Our platform has 1,000+ IIQE Paper 3 questions with detailed explanations, chapter-by-chapter practice, and full mock exams that simulate the real test.

👉 Access Full Question Bank

ExamPrep.hk's AI Focus Areas feature helps you focus your study time on your weakest areas.

Question Distribution by Chapter

Remember, IIQE Paper 3 distributes questions more evenly than Paper 1:

| Chapter | Topic | Est. Questions |

|---|---|---|

| Chapter 3 | Benefit Riders and Other Products | ~12 (24%) |

| Chapter 4 | Explaining the Life Insurance Policy | ~12 (24%) |

| Chapter 5 | Life Insurance Procedures | ~11 (22%) |

| Chapter 2 | Types of Life Insurance and Annuity | ~10 (20%) |

| Chapter 1 | Introduction to Life Insurance | ~5 (10%) |

All four major chapters (2–5) carry significant weight. Focus your practice across all of them for the best chance of passing. Learn exactly what to study within each chapter in our IIQE Paper 3 Difficulty Analysis.

Next Steps

Ready to continue your preparation?

- Read our Complete IIQE Paper 3 Study Guide for a proven 2-week study plan

- Check the Passing Score & Exam Format Guide to understand what you're aiming for

- Ready to book? Follow our IIQE Paper 3 registration guide

- Compare study methods in our resource comparison guide

- Start practicing with our full question bank for unlimited mock exams

IIQE Paper 3 Mock Exam FAQ

Ready to Put This Strategy Into Action? 💯

Join thousands of successful candidates who have passed their IIQE Paper 3 exam using our proven study methods.